HELOC vs cash-out refinance vs home equity loan

HELOC vs Cash-Out Refinance vs Home Equity Loan: A Practical Guide

When you need to access equity in your home, three common choices are a home equity line of credit (HELOC), a cash-out refinance, and a home equity loan. Each has different structures, costs, and risks. This guide explains how they work, when to consider each option, practical steps to compare them, and a brief FAQ to answer common questions.

How the three options work

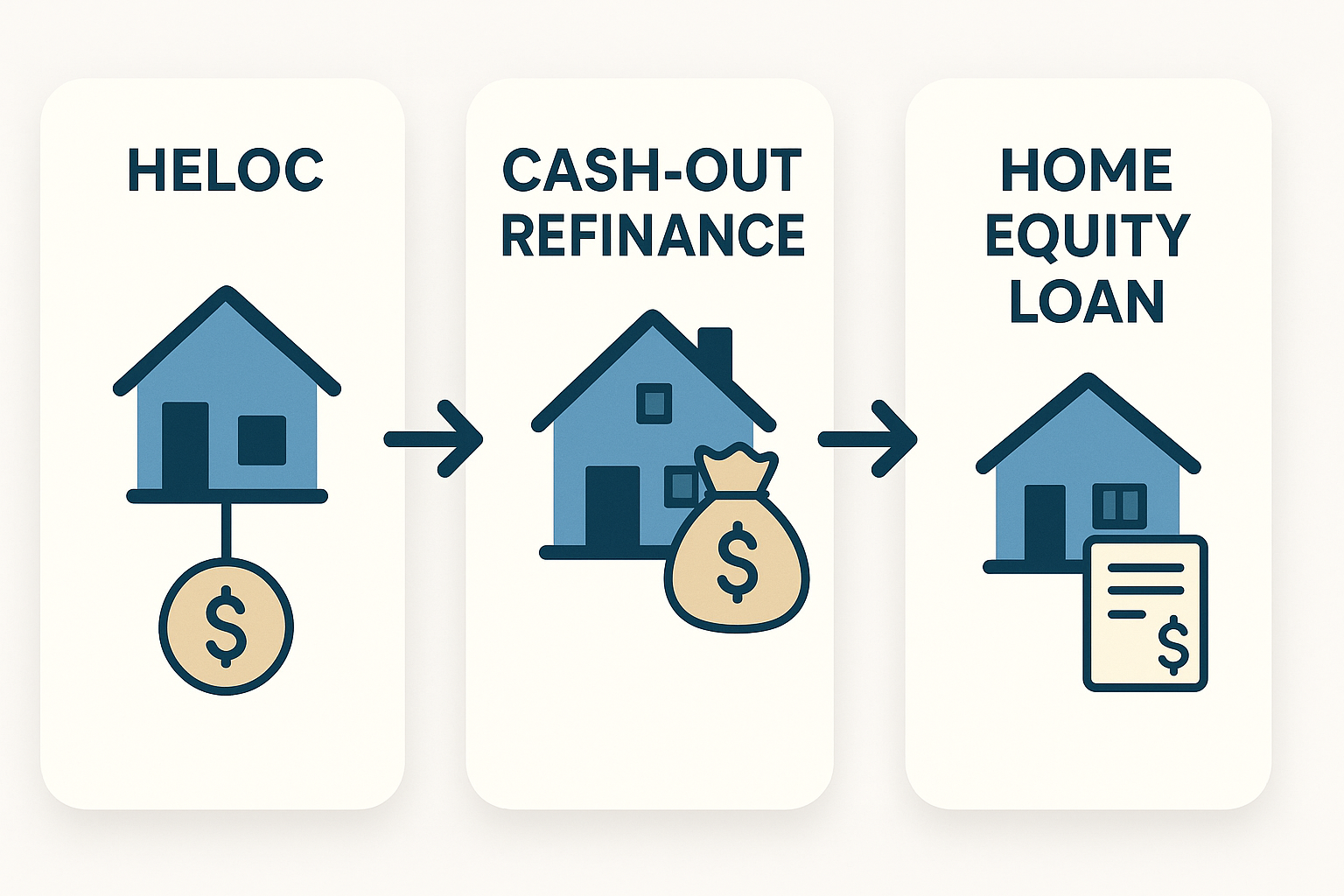

HELOC (Home Equity Line of Credit)

A HELOC works like a credit card secured by your home. The lender sets a maximum credit limit based on your home equity, and you can borrow as needed during a draw period (often 5–10 years). Interest rates are commonly variable, and monthly payments during the draw period may be interest-only or include principal and interest. After the draw period ends, the loan typically enters a repayment period (10–20 years) when you must pay principal and interest.

Cash-Out Refinance

A cash-out refinance replaces your existing mortgage with a new, larger mortgage. The new loan pays off your old mortgage, and you receive the difference in cash. This changes your loan term, interest rate, and monthly payment. Cash-out refinances are treated like a primary mortgage and usually have fixed rates and longer terms (15–30 years), though adjustable-rate options exist.

Home Equity Loan (Second Mortgage)

A home equity loan (sometimes called a second mortgage) provides a lump sum upfront with a fixed interest rate and fixed monthly payments. It is separate from your first mortgage and commonly has a fixed term (5–20 years). Repayment begins immediately on both principal and interest.

Key differences at a glance

- Structure: HELOC = revolving line of credit; Home equity loan = fixed lump sum; Cash-out refinance = replaces your first mortgage with a larger mortgage.

- Interest rates: HELOC = usually variable; Home equity loan = usually fixed; Cash-out refinance = typically fixed but can be adjustable.

- Closing costs: Cash-out refinance often has higher closing costs than HELOCs or home equity loans, but costs vary by lender and loan size.

- Monthly payments: Cash-out refinance may lower, raise, or keep the same monthly payment depending on rate and term; HELOC payments may be low initially (interest-only) then increase; home equity loan payments are predictable and fixed.

- Loan term and amortization: Cash-out refinance amortizes over the mortgage term; home equity loan has its own amortization; HELOC may have interest-only draw period followed by amortization.

- Use of funds: All three allow a variety of uses, but tax treatment of interest depends on how funds are used.

When to consider each option

Choose a HELOC if:

- You need a flexible source of funds over time (for example, ongoing home renovations or education costs).

- You want to borrow only what you need and avoid paying interest on unused funds.

- You are comfortable with a variable rate and possible payment variability.

Choose a cash-out refinance if:

- You can benefit from refinancing into a lower mortgage rate or longer term while accessing equity.

- You want a single mortgage payment and possibly a lower interest rate than a second mortgage.

- You need a large lump sum and prefer a fixed rate with long-term repayment.

Choose a home equity loan if:

- You need a defined lump sum and want the predictability of a fixed interest rate and fixed monthly payments.

- You prefer not to change or replace your existing mortgage.

- You do not want to deal with the variable rates and draw structure of a HELOC.

Costs, eligibility, and tax considerations

Costs and fees

All three options may involve fees: appraisal, application, title search, origination, and closing costs. Cash-out refinances often have higher total closing costs because they replace the existing mortgage and require underwriting comparable to a purchase. HELOCs and home equity loans may have lower upfront costs but check for annual fees, inactivity fees, or early termination fees. Compare APR (annual percentage rate) rather than just the quoted interest rate to include fees.

Eligibility and borrowing limit

Lenders determine maximum loan amounts based on your home’s value, existing mortgage balance, debt-to-income ratio, and credit score. Many lenders limit combined loan-to-value (CLTV) to 80%–90% of the home’s value, meaning you may be able to borrow up to that percentage across all liens on the property. Higher CLTV ratios or lower credit scores can raise interest rates or lead to denial.

Tax considerations

Interest deductibility for home equity loans, HELOCs, and cash-out refinances depends on how the funds are used and current tax law. Under rules established in recent tax law changes, interest is generally deductible only when the loan proceeds are used to buy, build, or substantially improve the taxpayer’s home that secures the loan. Using proceeds for general living expenses or debt consolidation may not be deductible. Tax rules change and individual circumstances vary; consult a tax professional for advice.

Practical steps to compare and choose

- Define your goal. Are you financing a single project, multiple projects over time, debt consolidation, or a major expense (education, medical, etc.)? The intended use influences the best product.

- Calculate how much you need. Include a buffer for unexpected costs but avoid borrowing more than necessary.

- Check your home equity and CLTV. Use recent home value estimates and subtract your outstanding mortgage balance to determine available equity.

- Review your current mortgage terms. Compare your current interest rate and remaining term with potential cash-out refinance terms to see if refinancing makes sense.

- Get multiple quotes. Shop several lenders for interest rates, APRs, and all fees. Ask for loan estimates and compare total costs over relevant time frames.

- Compare payment scenarios. For each option, look at monthly payments during draw and repayment periods (for HELOCs), and how the cash-out refinance or home equity loan affects your cash flow.

- Consider rate risk. If a HELOC has a variable rate, estimate payments under higher-rate scenarios. If you need predictability, a fixed-rate loan or cash-out refinance may be preferable.

- Check penalties and terms. Ask about prepayment penalties, draw period terms, annual fees for HELOCs, and whether the loan includes balloons or adjustable-rate resets.

- Factor in closing costs vs. payoff period. If you plan to carry the loan for a short time, higher closing costs on a cash-out refinance may not be worthwhile; consider a home equity loan or HELOC with lower upfront fees.

- Read documents carefully and consult professionals. Speak with lenders, a tax advisor, and—if needed—a financial planner to understand long-term implications.

Risks and trade-offs

- All three options use your home as collateral. Failing to repay can lead to foreclosure.

- Variable-rate HELOCs expose you to rising monthly payments if interest rates increase.

- Extending your first mortgage term through a cash-out refinance can lower monthly payments but increase total interest paid over time.

- Taking a second mortgage increases your monthly obligations and may complicate future refinancing or sale of the property.

- Using home equity to pay non-investment expenses reduces your ownership stake and may not improve your financial situation long-term.

When it might not make sense

Using home equity to fund discretionary spending that does not improve your financial position (for example, everyday consumption) can be risky. If you plan to move within a few years, a cash-out refinance with higher closing costs may not be recouped through rate savings. If you cannot tolerate payment uncertainty, avoid variable-rate HELOCs. Carefully assess alternatives such as personal loans, borrowing from retirement plans (with caution), or saving until you can pay in cash.

Brief FAQ

Which option is usually the cheapest?

There is no single cheapest option; it depends on rates, fees, and how long you expect to carry the loan. Cash-out refinances can offer lower interest rates because they replace the first mortgage, but they typically have higher closing costs. HELOCs may have lower upfront costs but variable rates. Compare APR and total costs for your expected timeframe.

Can I refinance a HELOC into my mortgage later?

Yes. You can consolidate a HELOC into a new mortgage via a refinance or cash-out refinance, subject to lender approval and costs. This can convert variable-rate debt to a fixed-rate mortgage but will involve closing costs and underwriting.

Is interest on HELOCs or home equity loans tax-deductible?

Interest deductibility depends on how you use the loan proceeds and current tax law. Generally, interest is deductible only when funds are used to buy, build, or substantially improve the home securing the loan. Consult a tax advisor for your situation.

How does borrowing affect selling the house?

If you sell the house, outstanding mortgage balances, home equity loans, and HELOCs must be paid from sale proceeds. Having additional liens can reduce your net proceeds and may complicate transactions if liens approach the home’s value.

Will applying affect my credit score?

Yes. Loan applications typically result in a hard credit inquiry, which can cause a small, temporary score dip. Having additional debt increases your overall balances and can affect your credit utilization and score. Timely payments can help maintain or improve your score over time.

Final considerations

Choosing between a HELOC, a cash-out refinance, and a home equity loan depends on your borrowing purpose, timeline, desire for payment stability, and tolerance for rate risk. Start by clarifying your goal, getting multiple loan estimates, and comparing APRs and fees over the period you expect to carry the debt. Keep in mind tax implications and the fact that your home secures these loans—evaluate risks carefully and consult financial or tax professionals as needed.