Mortgage Refinance Rates Dip to 6.69% for 30-Year Fixed Loans in Mid‑2025

Mortgage refinance rates dip to 6.69% for 30‑year fixed loans

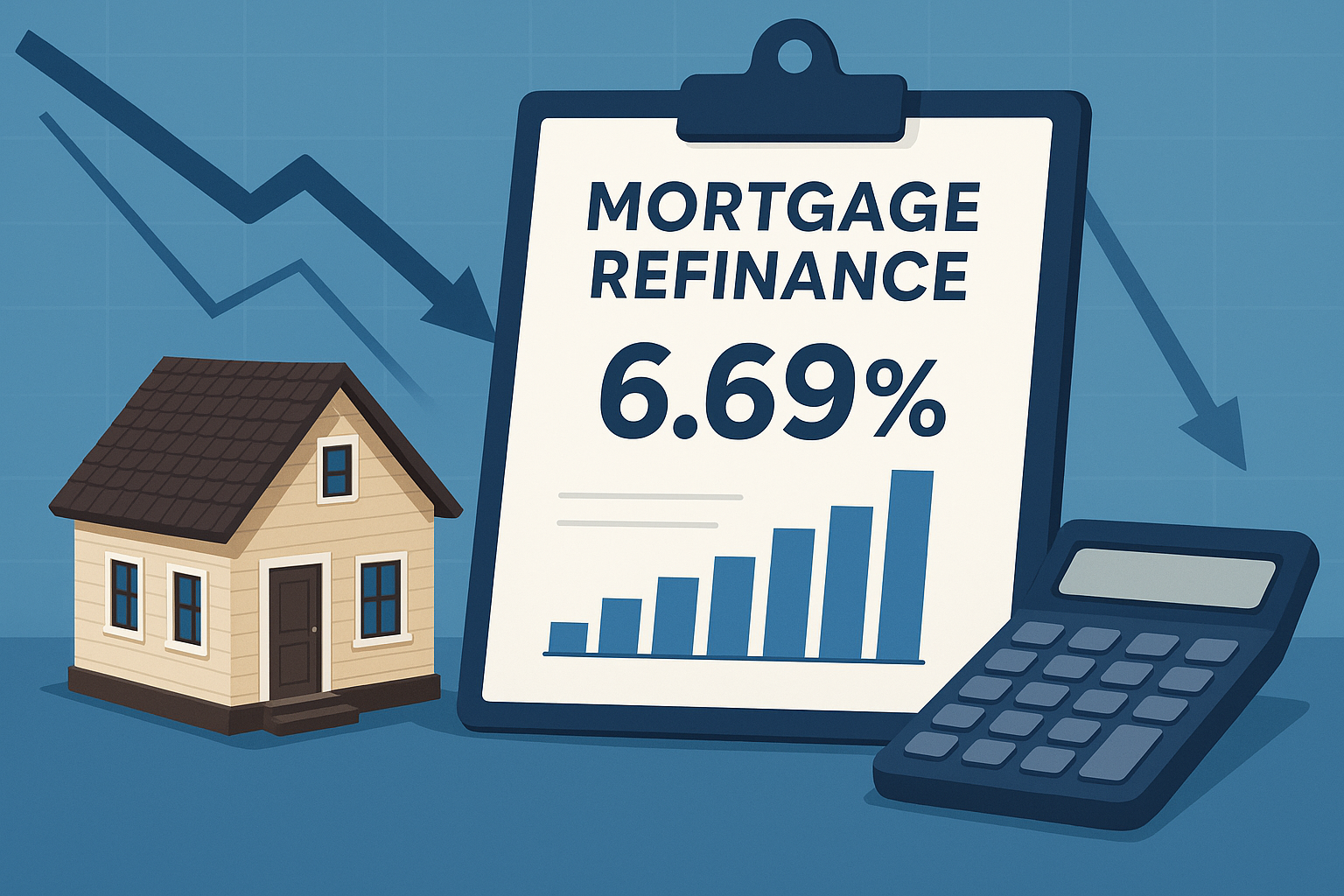

Mid‑2025 saw a modest downward move in long‑term mortgage costs, with 30‑year fixed refinance rates falling to about 6.69%, according to a market summary published Aug. 11, 2025. The report notes the easing came amid shifting bond yields and a broader pullback in some benchmark interest rates that influence mortgage pricing.

What the AInvest summary reports

The AInvest piece tracking refinance rates for mid‑2025 highlights a retreat in 30‑year fixed refinance rates to roughly 6.69%. The article frames this as part of a short‑term easing trend after a period of higher rates earlier in the year. While day‑to‑day mortgage pricing can move with Treasury yields and lender margins, the AInvest snapshot reflects market conditions that may make refinancing more attractive for some homeowners.

Recent context and how rates have moved

Mortgage rates have been volatile in 2024–2025 as markets reacted to inflation readings, Federal Reserve policy signals and changes in long‑term bond yields. The mid‑2025 dip to the high‑6% range followed several months when 30‑year fixed rates were higher, and it represents a partial reversal rather than a sustained low‑rate environment. Lenders typically set refinance pricing based on a mix of Treasury yields, credit spreads and pipeline dynamics, so small moves in those inputs can change advertised refinance rates.

Who stands to benefit from the decline

Homeowners with existing mortgages at materially higher rates may find refinancing appealing if the new rate and loan costs produce meaningful savings. Borrowers most likely to benefit include:

- Those with adjustable‑rate mortgages that are resetting to higher payments.

- Owners with 30‑ or 15‑year loans issued during earlier, higher‑rate periods.

- Borrowers who can qualify for competitive pricing based on credit score, loan‑to‑value and documentation.

However, whether refinancing is worthwhile depends on individual circumstances: the size of the rate reduction, remaining loan term, closing costs and how long the homeowner plans to keep the property.

How homeowners should evaluate a refinance now

Before moving ahead, homeowners should run the numbers and compare options. Key steps include:

- Calculate the break‑even period: divide total refinance costs (closing fees, appraisal, points) by the expected monthly savings to estimate how long it takes to recoup costs.

- Compare fixed‑rate terms: a lower rate on a longer remaining term can reduce monthly payment but may extend interest costs over time; a shorter term usually increases monthly cost but lowers total interest paid.

- Check eligibility and quotes from multiple lenders: rates vary by lender, borrower credit profile and loan size; shop and obtain Good Faith Estimates or Loan Estimates for apples‑to‑apples comparisons.

- Consider alternative products: for some borrowers, a HELOC or a rate‑and‑term refi (versus cash‑out) could be preferable depending on goals and costs.

Risks and factors that could change the picture

Mortgage pricing remains sensitive to macro developments. Factors that could push rates back up or down include:

- Federal Reserve policy signals and interest‑rate expectations.

- Movements in the 10‑year Treasury yield, which closely influence long‑term mortgage pricing.

- Credit conditions and lender capacity—when lenders pull back or grow more aggressive, spreads change.

- Unexpected economic data (inflation, employment, growth) that shifts investor expectations.

Because these drivers can shift quickly, timing a refinance for the absolute best rate is difficult; many financial advisers recommend focusing on whether the projected savings meet personal financial goals rather than trying to chase daily rate fluctuations.

Why it matters

Even modest declines in 30‑year refinance rates can unlock meaningful monthly and lifetime interest savings for homeowners who previously locked in significantly higher rates. When rates move into the lower high‑6% range, some borrowers who had been priced out of refinancing may become viable candidates again. For the housing market more broadly, a pickup in refinancing activity can affect consumer cash flow, spending and the mortgage servicing market.

Bottom line

The mid‑2025 dip in 30‑year fixed refinance rates to about 6.69% represents a potentially useful window for some homeowners to review refinancing options. It is not a dramatic return to the ultra‑low rates of earlier cycles, but for borrowers with higher current rates, the move may change the calculus. As always, homeowners should compare multiple lender offers, run a break‑even analysis and weigh the long‑term tradeoffs of changing loan terms.